Tax Disclaimer: This guide covers general educational information about potential tax deductions for portable power stations used in business. Tax laws vary by jurisdiction and change frequently — this is not professional tax advice. Always consult a qualified CPA, tax attorney, or enrolled agent before claiming any deduction. Improper deductions can trigger audits, penalties, and interest.

A portable power station purchased for legitimate business use can qualify as a deductible expense under several IRS categories. Depending on your situation, it may be treated as equipment eligible for Section 179 immediate expensing, depreciated over time under MACRS, expensed under the de minimis safe harbor, or included as part of a home office setup.

The key word is legitimate. The IRS allows deductions for “ordinary and necessary” business expenses — meaning the expense is common in your industry and helpful for your operations. A portable power station powering tools on a construction site or running a POS system at a farmer’s market meets that test. One that sits in your garage for the occasional camping trip and happens to get plugged in during a work-from-home day does not.

The burden of proof is on you. That means keeping purchase receipts, maintaining usage logs, calculating honest business-use percentages, and being able to articulate why the equipment matters to your operations. Even a perfectly legitimate deduction falls apart without documentation.

This guide walks through which business uses qualify, how Section 179 and depreciation compare, what documentation the IRS expects, and how home office and mixed-use scenarios work. The goal is to help you have a more informed conversation with your tax advisor — not to replace one.

For operational context on specific use cases, see our guides on portable power stations for construction sites, food trucks, photographers, and outdoor weddings and events.

Legitimate Business Use Categories

A portable power station becomes a viable deduction only when it’s genuinely tied to how you earn money. The stronger and more direct the connection to revenue-generating work, the easier the deduction is to defend. The clearest cases involve mobile operations where on-site power is necessary — not merely convenient — for delivering services.

Mobile Business Operations

Food trucks, event vendors, photographers, videographers, and construction contractors frequently operate where grid power is unreliable or nonexistent. For these businesses, a portable power station is core infrastructure, not a nice-to-have.

Food truck example: A mobile food vendor purchases two high-capacity stations totaling $3,000 to power refrigerators, freezers, POS systems, and lighting at markets held in parking lots and parks without shore power. Revenue from these events represents a significant portion of annual sales. The vendor retains purchase receipts, event calendars, and revenue tied to powered events. That’s a clean, defensible business expense — eligible for Section 179 or depreciation, with strong documentation linking the equipment directly to income.

Photographer example: A professional photographer buys a $1,500 station to support full-day outdoor shoots and destination weddings — running camera chargers, a laptop, LED lighting, and occasionally a small printer for on-site proofs. She logs each job where the station is used and ties it to client invoices. The same unit goes on family camping trips three or four times a year, so she deducts only the business-use percentage. That’s honest, documented, and defensible.

Construction and Trades

Contractors increasingly use battery-based power for jobs where generator noise isn’t acceptable — residential remodels in neighborhoods with noise restrictions, HOA-regulated areas, or clients who simply prefer quiet. Running cordless tool chargers, work lights, and small compressors from a portable station is an ordinary and necessary expense for that type of work. For more on this use case, our construction power station guide covers operational considerations in detail.

Home Office Use

This one requires more care. A self-employed consultant with a qualifying home office might purchase a portable power station to keep computers, monitors, and networking gear running during outages — maintaining the ability to bill clients and meet deadlines. If the station lives in the office and exclusively powers work equipment, treating it as 100% business-use equipment is reasonable.

But if that same station regularly powers the living room TV, kitchen appliances, and entertainment systems during storms, you’re looking at mixed use. Be honest about the split. An 80% business claim for a unit that spends half its time powering the family room during outages is a problem waiting to happen.

Business Travel and Field Work

Territory sales reps working from their cars between rural meetings, consultants at client sites with unreliable power, field technicians running diagnostic equipment — these are all strong business cases when documented properly. The common thread is that the power station directly enables revenue-generating activity that wouldn’t happen without it.

Events and Entertainment

DJs, wedding planners, and production companies often have the cleanest fact patterns. If an outdoor event literally cannot proceed without portable power, and that power is part of the service you’re selling to clients, the “ordinary and necessary” test is satisfied about as clearly as it gets. See our outdoor weddings and events guide for recommendations on which units handle event loads.

The Business Purpose Principle

Across all categories, what matters is genuine integration into operations, regular use in revenue-generating activities, and a credible paper trail. A deduction based on occasional or marginal business use — with the equipment primarily serving personal needs — will be difficult to defend. If you’re honest with yourself about why you bought it and how you actually use it, you’ll know whether the deduction holds up.

Section 179 vs. Depreciation vs. De Minimis Safe Harbor

Once you’ve established legitimate business use, the next question is how to deduct the cost. There are three main paths, and each fits different situations.

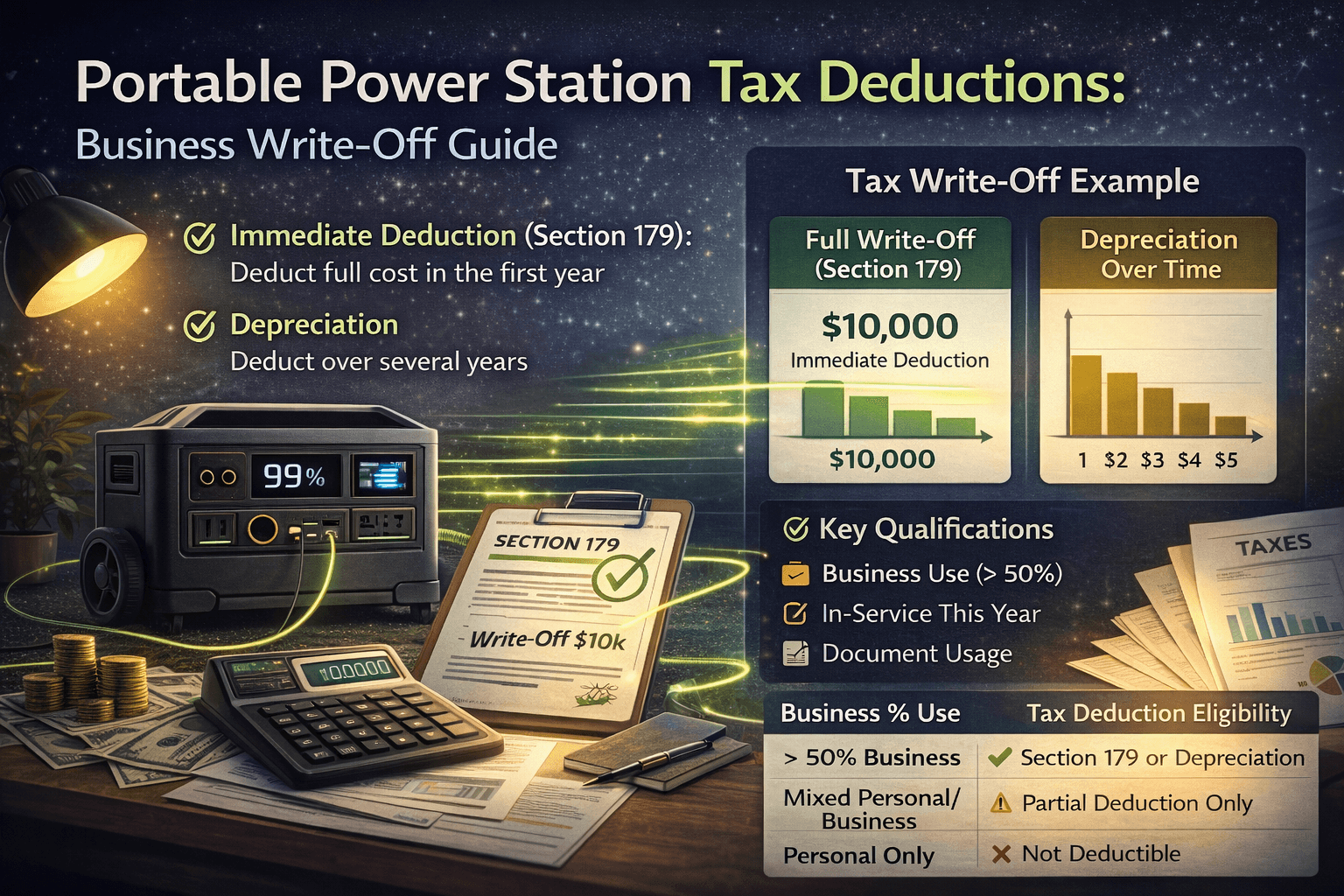

Section 179: Immediate Expensing

Section 179 lets you deduct the full cost of qualifying business equipment in the year you put it in service, rather than spreading the deduction over multiple years. Portable power stations — as tangible personal property used in a trade or business — generally qualify.

Key requirements:

- The equipment must be used more than 50% for business

- Your total Section 179 deduction can’t exceed your taxable business income (you generally can’t use it to create a net loss)

- For tax years beginning in 2025, the maximum Section 179 deduction is $2,500,000, with phase-out beginning when total qualifying property exceeds $4,000,000 (these limits were significantly increased by the One Big Beautiful Bill Act signed in mid-2025)

For context, these dollar caps are designed for businesses buying hundreds of thousands in equipment. A $1,500 portable power station won’t come anywhere near the limit. The practical constraint for most small operators is the taxable income limitation — you need enough business income to absorb the deduction.

Simple example: A sole proprietor with $50,000 of taxable business income buys $3,000 of portable power equipment used 100% for business. By electing Section 179, she deducts the full $3,000 in the year of purchase, reducing business income to $47,000. At a combined 25% federal and state rate, that saves roughly $750 in taxes immediately.

Section 179 is attractive because it accelerates the tax benefit into the current year. For most small business owners buying portable power stations, it’s the most straightforward option.

MACRS Depreciation: Spreading the Deduction

If Section 179 isn’t elected or can’t be fully used due to income limitations, the default is MACRS (Modified Accelerated Cost Recovery System) depreciation. Most portable power station equipment falls into the 5-year or 7-year property class, with deductions front-loaded in the early years under a declining balance method.

Spreading deductions can sometimes be strategic. If current-year income is low but higher income is expected in future years, deferring part of the deduction to align with higher tax brackets can yield more total savings. Complex situations involving multiple large equipment purchases should be modeled with a tax professional rather than handled with rules of thumb.

It’s also worth noting that bonus depreciation — which allows accelerated write-offs beyond Section 179 — was restored to 100% for qualifying property acquired and placed in service after January 19, 2025, under the One Big Beautiful Bill Act. Your CPA can help determine whether Section 179, bonus depreciation, or a combination produces the best result for your specific situation.

De Minimis Safe Harbor: Simplest Option for Smaller Purchases

For lower-cost equipment, the de minimis safe harbor election can eliminate the need for either Section 179 paperwork or depreciation tracking altogether. Under this rule, many taxpayers can expense items costing up to $2,500 per invoice or per item (if you lack an applicable financial statement) or up to $5,000 per item (if you have audited financial statements).

For a $500–$2,000 portable power station — which covers most units in the under $300 and under $500 categories — this is often the simplest path. You expense it as a regular business cost without formal depreciation schedules or Section 179 elections.

Important: To use this safe harbor, you need a written accounting policy in place at the start of the tax year treating items below the threshold as expenses, and you must make the election annually by attaching a statement to your tax return.

Which Method Should You Choose?

It depends on the cost of the equipment, your overall spending, income level, and long-term planning. Here’s a rough decision framework:

- Station costs $2,500 or less: De minimis safe harbor is usually simplest

- Station costs more than $2,500 and you want the full deduction this year: Section 179 (subject to the income limitation)

- Current income is low, expect higher income soon: Consider MACRS depreciation to shift deductions to higher-rate years

Because these rules interact with other parts of the tax code — and particularly with bonus depreciation rules that change frequently — confirm the best approach with your CPA before filing.

Documentation Requirements

No matter which deduction path you take, documentation is what makes it defensible. The IRS gives far more weight to records created at or near the time of use than to reconstructions assembled under audit pressure.

Purchase Records

Keep the basics: original invoice or receipt showing seller, date, model, and price. A credit card statement or bank record confirming payment. Optionally, save product specifications that explain what the station does and its capabilities — this helps establish that the item is what you say it is.

Business Use Log

For mixed-use equipment especially, a contemporaneous log is essential. This doesn’t need to be complicated — a simple spreadsheet, calendar notation, or even a notebook works — as long as it’s consistent and tracks:

- Date and location of use

- Business activity supported (job site, client event, shoot location)

- Approximate duration of use

- Devices or systems powered (tools, POS, lighting, computers)

- Client, project, or invoice reference connecting the use to revenue

Business Justification Memo

A one-page memo explaining why you need a portable power station for your specific business is powerful documentation. “I run a mobile food vending business operating at 30+ outdoor events per year at locations without shore power. Portable power stations enable refrigeration, POS operations, and lighting — without them, I can’t operate at these revenue-generating events.” That kind of clear, specific statement provides context and demonstrates forethought.

Mixed-Use Percentage Calculation

If the station serves both business and personal purposes, your logs need to support the split. Example: 180 hours of business use and 60 hours of personal use during the year yields a 75% business-use percentage. Apply that percentage to Section 179 elections, depreciation, and operating expenses. The IRS expects the percentage to reflect reality, not aspiration.

Well-organized, contemporaneous records turn a potential audit into a straightforward document review. Without them, even a legitimate deduction becomes difficult to defend.

Home Office Deductions

Home office deductions are among the most scrutinized claims on tax returns, so portable power in this context requires extra care.

Qualifying Your Home Office First

Before the power station matters, the office itself must qualify. The space must be used regularly and exclusively for business, and must be your principal place of business, a location where you regularly meet clients, or a separate structure used for work. If the “office” is your kitchen table that doubles as homework central, neither the office nor the power station qualifies.

Adding Portable Power to a Qualifying Office

A consultant who relies on desktop computers, monitors, and networking gear to serve clients might purchase a portable power station specifically to maintain operations during outages. If that station lives in the qualifying office and only powers office equipment, claiming it as 100% business equipment is reasonable.

The problem arises when the same device regularly gets dragged to the living room during storms or powers kitchen appliances. In that situation, a 100% business claim isn’t credible. Use honest logs, apply a conservative allocation (50–70% depending on actual patterns), and keep the documentation airtight.

Simplified vs. Actual Expense Method

The simplified home office deduction uses a flat rate based on square footage and generally doesn’t accommodate equipment-specific deductions. To claim a portable power station as part of your home office, you’ll typically need to use the actual expense method and track a broader set of home-related costs. Your CPA can advise which method produces a better result overall.

Because home office deductions are a known audit trigger, conservative and honest claims are worth more than aggressive positions. Only claim a home office that genuinely meets IRS requirements, and only include portable power that’s genuinely part of that office’s infrastructure.

Audit Risk Management

Think about every deduction in terms of audit defensibility, not just immediate savings. The goal is to claim everything you’re legitimately entitled to while keeping your return clean and well-supported.

Be Realistic About Percentages

Claiming 100% business use for equipment that has obvious personal value — like a portable power station kept at home — raises questions unless there’s a clear explanation (exclusive use at commercial job sites, for instance). For mixed-use items, base percentages on actual logs and err slightly conservative. Good faith counts.

Build Documentation Into Your Workflow

Don’t wait until tax time to reconstruct a year of usage from memory. Calendar entries for events, job site logs, project management systems, and even phone photos of the station at work sites all build a real-time narrative of business use. This is far more credible than a retroactive spreadsheet.

Watch the Overall Profile

A single portable power station deduction won’t trigger an audit on its own. But when combined with aggressive home office claims, heavy vehicle write-offs, and large travel deductions, it contributes to a return profile the IRS considers higher risk. Moderation and solid justification across the board keeps you in a comfortable zone.

Know When to Get Help

If you operate multiple entities, have significant equipment purchases relative to income, or have been audited before, professional guidance isn’t optional. A CPA or enrolled agent costs a fraction of what an adverse audit examination could, and they can position your deduction strategy within a broader risk-management framework.

Business Structure Considerations

Your entity type affects how the deduction flows through your tax return, though the underlying rules for Section 179, depreciation, and business use are largely the same across structures.

Sole proprietors report everything on Schedule C. Equipment costs go on Form 4562, and deductions directly reduce taxable income and self-employment tax. This is the most straightforward setup.

Partnerships and multi-member LLCs (taxed as partnerships) deduct equipment at the entity level and pass Section 179 elections through to partners via Schedule K-1. Individual partners must have sufficient income to fully use the passed-through deduction.

S corporations work similarly — deductions flow through to shareholders. C corporations take deductions at the corporate level, reducing corporate taxable income. The benefit to owners comes indirectly through higher after-tax profits.

Entity selection has implications far beyond a single equipment purchase — liability protection, payroll tax exposure, administrative costs — so don’t restructure just to optimize one deduction. But understanding how your current structure handles equipment deductions helps you set realistic expectations when planning purchases.

Frequently Asked Questions

Can I deduct a portable power station bought for home emergency backup?

Almost certainly not. A station kept primarily for home emergency backup — powering your refrigerator, lights, and phone during outages — is a personal expense. The IRS doesn’t allow deductions for personal living costs, even when they incidentally make working from home easier.

The deduction only works when the primary purpose is business-related: powering a qualifying home office, supporting mobile operations, or enabling on-site services for clients. Occasional business use of a unit bought mainly for household preparedness doesn’t change its fundamental character.

If the unit genuinely serves both roles, a mixed-use approach with documented allocation can work — but be honest about the split. If you bought it because hurricane season scared you and work use is an afterthought, treat it as a personal expense.

What about portable solar panels — are they deductible too?

The same principles apply. If solar panels are purchased for business use — charging your power station at job sites, events, or during client work — they’re deductible as business equipment under the same rules. Documentation and business-use requirements are identical. See our solar panel guide for operational guidance on pairing panels with power stations.

Is a $500 power station worth the hassle of deducting?

Potentially yes, especially using the de minimis safe harbor. The administrative burden is minimal — you need a written accounting policy and a statement attached to your return. At a 25% combined tax rate, a $500 deduction saves you $125. Not life-changing, but the effort is minimal if the business use is genuine and you’re already filing business taxes.

Can I deduct a power station I bought last year but didn’t claim?

Possibly. If the station was placed in service in a prior tax year and you didn’t claim a deduction, you may be able to file an amended return (Form 1040-X) or, in some cases, adjust depreciation going forward. This is exactly the kind of situation where a tax professional’s guidance is worth the cost — the rules around amended returns and method-of-accounting changes have specific requirements and deadlines.

Key Takeaways

Portable power stations used for genuine business purposes can be deducted as equipment — through Section 179 immediate expensing, MACRS depreciation, or the de minimis safe harbor for smaller purchases. The foundation of any defensible claim is strong documentation, honest business-use percentages, and clear business necessity.

Mobile businesses, event professionals, contractors, and some home office users have the strongest cases. Personal emergency backup, with incidental business use, is almost never deductible.

Treat your tax reporting the way you’d want it to look if the IRS asked questions: honest, well-documented, and clearly tied to how your business actually operates. Then work with your CPA or enrolled agent to choose the best combination of deduction methods for your situation.

Final reminder: This guide is educational only. Tax rules change, interpretations vary, and your specific circumstances matter enormously. Always consult a qualified tax professional before claiming any portable power station deduction.